Targeted EPF Withdrawals: Weighing the Risks and Benefits

The Employees Provident Fund (EPF) has long been a pillar of retirement planning in Malaysia. However, the economic challenges posed by the COVID-19 pandemic have sparked a debate over targeted EPF withdrawals as a means to alleviate financial distress. While some see this as a necessary relief, the Finance Ministry warns of the potential long-term repercussions, especially the risk of insufficient retirement savings.

Understanding the Rationale for Targeted EPF Withdrawals

Advocates for targeted EPF withdrawals argue that such measures could offer crucial financial support to those hit hardest by the pandemic. This could include covering essential costs like housing, food, and healthcare, potentially preventing individuals from falling into debt or having to liquidate assets.

Examining the Concerns of the Finance Ministry

The Finance Ministry’s apprehensions center on the possible depletion of retirement funds. Immediate relief might come at the cost of future financial security, particularly as Malaysia already grapples with a retirement savings deficit. A significant portion of EPF members under 55 have less than RM10,000 in savings, underscoring the gravity of the situation.

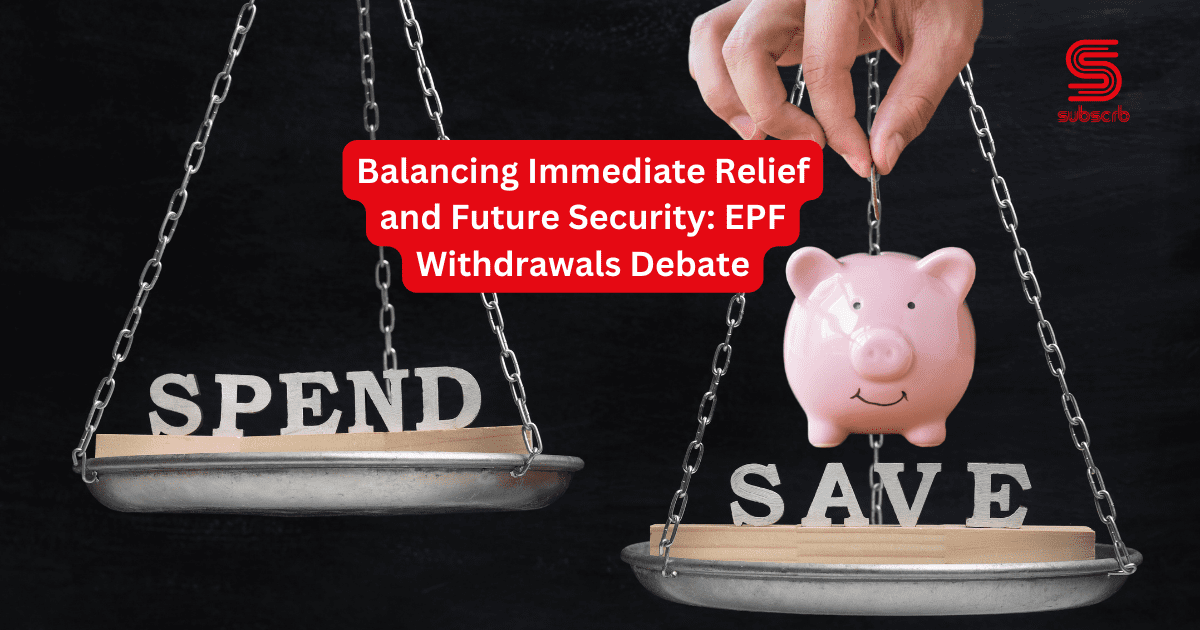

Balancing Short-Term Needs with Long-Term Sustainability

This debate highlights the need to strike a balance between providing immediate aid and ensuring the long-term viability of retirement savings. While addressing current financial challenges is vital, preserving the future economic stability of individuals is equally important.

Alternative Measures to Address Financial Hardship

In light of the risks associated with targeted EPF withdrawals, alternative strategies should be considered:

- Expand Targeted Financial Assistance Programs: Enhancing existing financial aid programs could offer more specific support, reducing dependence on EPF funds.

- Enhance Financial Literacy and Counseling: Improving financial education and offering counseling can help individuals make better financial decisions.

- Encourage Employer Support: Employer-led financial assistance and support programs could provide a safety net for employees, preserving their retirement savings.

Conclusion

Deciding on targeted EPF withdrawals demands a careful evaluation of both immediate and long-term impacts. While the need for short-term relief is clear, prioritizing long-term financial security is essential. By exploring alternative solutions and promoting financial prudence, Malaysia can navigate these challenging times without compromising the future financial well-being of its citizens.